3 min read

eIDAS – Digitisation of the on-boarding process Part 2 - The Process

In Part 1 of this series, we looked at the objectives or motives behind having an eIDAS-enabled digital onboarding process. In Part 2, we look at the...

3 min read

In Part 1 of this series, we looked at the objectives or motives behind having an eIDAS-enabled digital onboarding process. In Part 2, we look at the...

2 min read

The EU single market produces an unmatched € 15trillion worth of goods and services annually. Such a large and unified market presents many...

3 min read

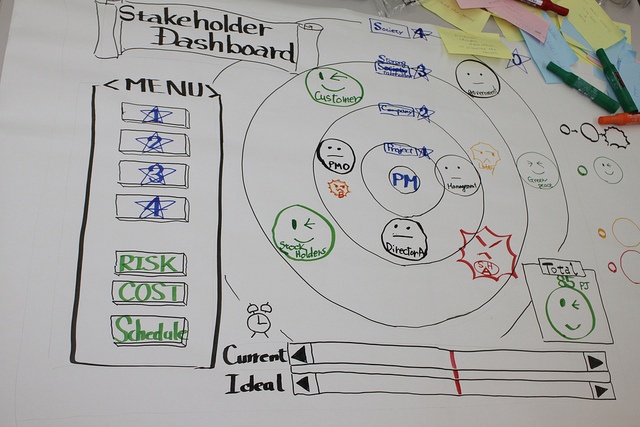

The initial client on-boarding procedure is crucial for both banks and their clients. For banks, the efficiency and speed of the process can leave a...

3 min read

The ultimate aim of regulations like eIDAS is the creation of a true Digital Single Market (DSM). eIDAS plays its role by providing the necessary...

3 min read

With each passing year, the volume of international trade in goods and services keeps rising. With all of this trade, however, comes an associated...

3 min read

The eIDAS regulation is a key foundational stone in creating the pan-European Digital Single Market. It provides the essential elements to build a...

3 min read

In Part 1 of our article, we briefly summarised the challenges faced in the uptake of eIDAS services for SMEs. A study conducted for the European...

3 min read

The EU has launched a number of initiatives to realize the aim of creating a unified Digital Single Market. The Connecting Europe Facility (CEF) is a...

3 min read

The Delegated Regulation on Regulatory Technical Standards (RTS) by the European Commission aims to facilitate Strong Customer Authentication (SCA)...