1 min read

Unveiling Obsidian: Next-Gen Payment Platform for the Cloud Era

We are delighted to announce the launch of Obsidian payment platform, a cutting-edge digital payments solution for issuers designed to meet the...

1 min read

We are delighted to announce the launch of Obsidian payment platform, a cutting-edge digital payments solution for issuers designed to meet the...

4 min read

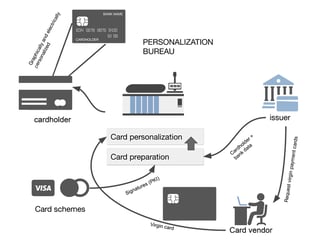

EMV Personalization of a payment card is the process of writing data to the card in order to make it ready for use. This includes loading the card...

4 min read

The “Four Corners” model, also called the “Four Party Scheme”, is utilized in almost all standard card payment systems across the globe. Here, we...

3 min read

EMV Personalization is a process used to get card data into cards, mobile phones, and wearables. The process includes a variety of complicated...

4 min read

In the “four corner model”, acquirers are apparently the less active party as their role seems ‘only’ to forward the transaction flow originating...

3 min read

An issuer is one of the corners in the ‘four corner’ model. An issuer is a financial organization (e.g. a bank) that produces payment cards and...

3 min read

The EMV personalization data processing in itself is not the topic of this article, we will instead focus on the cryptographic schemes involved in...

4 min read

Cardholders (or consumers) are one of the corners of the ‘four corner’ model in the payment card world. Here we take a brief look at the payment...

5 min read

This article talks about how different factors and controls can affect the strength and effectiveness of a cryptographic system's security. It gives...